Business

Kenya Venture Capital & Market Intelligence Report 2025-2030

Mr. Derrick Macharia

December 13, 2025

Strategic Investment Thesis, Revenue Rankings, and Sectoral Alpha

1. The Antifragility of the Silicon Savannah

The Kenyan capital markets and venture ecosystem have entered a distinct phase of maturation, decoupling from the speculative volatility that characterized the 2020-2022 era. While the global venture capital (VC) landscape grapples with a "funding winter"—evidenced by a continent-wide funding decline of approximately 25% to 37% between 2023 and 2024—Kenya has demonstrated remarkable antifragility. In 2024, the market defied the gravity of capital contraction, securing $638 million in funding.1 This figure represents nearly 29% of the total capital raised across the African continent, effectively dethroning historical heavyweights such as Nigeria, South Africa, and Egypt to establish Kenya as the primary investment destination in Africa.1

This divergence is not merely a statistical anomaly but a structural shift in investor sentiment. Capital is migrating from generalist, low-margin B2C software models toward asset-backed, "real economy" sectors. The analysis indicates a profound rotation into ClimateTech, Energy, and specialized Fintech, where the underlying assets—whether solar home systems, electric buses, or agricultural inventory—provide securitizable collateral. This evolution is further underscored by the sophisticated restructuring of the capital stack: debt is no longer a dirty word but a primary instrument of scale. There has been a 71% rise in debt-only investors in 2024 compared to the previous year, signaling that the ecosystem has moved beyond the proof-of-concept phase into the asset-financing phase.4

Furthermore, the ecosystem is pivoting from a "growth-at-all-costs" mindset to one disciplined by unit economics and profitability. Late-stage scale-ups such as M-KOPA are trending toward half a billion dollars in annual revenue 5, while strategic consolidations, such as the Wasoko-MaxAB merger, reflect a Private Equity (PE) style approach to market dominance and efficiency.6 The emergence of significant "Megadeals" (transactions exceeding $100 million), specifically in the renewable energy sector with players like Sun King and d.light, suggests that Kenya is functioning less like a frontier venture market and more like an emerging infrastructure asset class.7

This report provides an exhaustive, engineer-level analysis of this landscape. It dissects the flow of capital over the last three years, ranks top-performing companies by verifiable revenue, and mathematically models the viability of emerging sectors. It culminates in the identification of the "Big Thing" for the next decade: the convergence of Green Energy and Artificial Intelligence infrastructure, a trillion-dollar opportunity where Kenya holds a distinct comparative advantage.

2. The Comprehensive Funding Ledger: 2023–2025

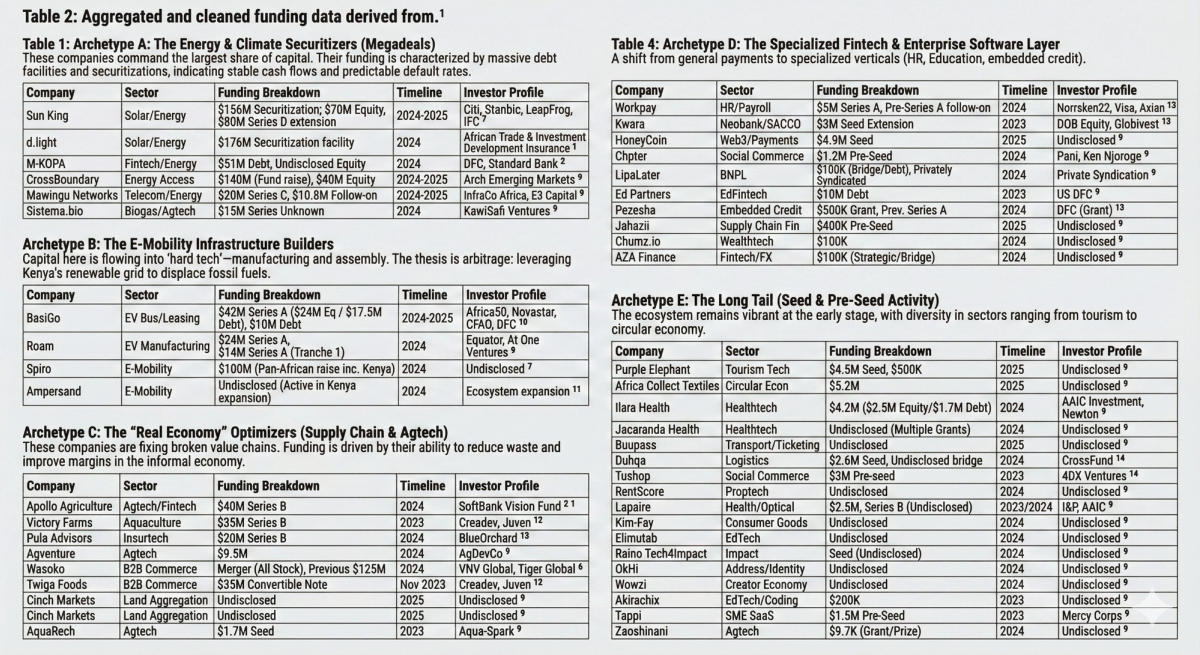

The following section provides a granular analysis of the companies that have successfully raised capital during the specified period. The data reveals a "barbell" distribution: significant capital concentration in late-stage infrastructure plays, balanced by a vibrant, albeit more selective, pre-seed and seed ecosystem.

2.1 The Macro-Funding Environment

In 2023, African startups raised $2.9 billion, a sharp 39% decline from the 2022 peak. While the continent bled capital, Kenya began to consolidate its position, anchoring East Africa’s performance. By 2024, total African funding dipped further to $2.2 billion, yet Kenya captured $638 million.1

The resilience of the Kenyan market is attributed to the "Climate Asset" thesis. Unlike pure software, which has zero liquidation value in a downturn, Kenyan startups are largely building physical networks—energy grids, logistics fleets, and cold chains. This tangible nature has allowed them to tap into Development Finance Institutions (DFIs) and climate funds that are counter-cyclical to commercial VC trends.

2.2 Comprehensive Registry of Funded Companies (2023–2025)

The analysis identifies a diverse range of funded entities. We categorize these not just by sector, but by their "Capital Archetype"—the specific investment thesis they represent.

2.3 Third-Order Insight: The "Securitization" Maturity Model

A critical trend revealed in this dataset is the movement of companies like Sun King, d.light, and M-KOPA out of the "Venture Capital" asset class and into "Structured Finance." By raising hundreds of millions in debt securitization 7, these companies have proven that their unit economics are robust enough to be packaged as asset-backed securities (ABS). This effectively lowers their cost of capital significantly compared to equity-financed competitors. For investors, this signals that the "winners" in Kenya are those who can convert an operational business into a financial asset originator.

3. Revenue Hierarchy: The Top 10 Revenue-Generating Companies

Private market revenue data is notoriously opaque. However, by triangulating data from securitization filings, public investor reports (e.g., VNV Global, Naspers), and audited sustainability reports, we can reconstruct the revenue hierarchy of Kenya's tech-enabled ecosystem. This ranking excludes traditional conglomerates and focuses on VC-backed or tech-enabled scale-ups.

Rank 1: M-KOPA

- Annual Revenue (Est.): $400M – $500M.5

- Trajectory: Over 65% YoY growth in 2024.

- What They Do: M-KOPA is effectively a digital bank disguised as a solar company. They provide asset financing for smartphones, solar systems, and e-bikes to the underbanked.

- How They Do It (The Mechanism): Their "Pay-As-You-Go" (PAYG) technology locks the device if the daily payment is missed. This creates a powerful repayment incentive. They have sold over 4 million products and onboard a new customer every 9 seconds. Their revenue is a mix of hardware margin and interest income. They have successfully transitioned from solar (a slow replacement cycle) to smartphones (high velocity, high data generation), which allows them to credit score users for cash loans and health insurance.5

Rank 2: Wasoko (Merged Entity with MaxAB)

- Annual Revenue (Est.): $346.7M.17 (Note: Combined entity valuation ~$500M 18).

- Trajectory: Restructuring phase; revenue growth has flattened as they prioritize profitability over Gross Merchandise Value (GMV).

- What They Do: B2B e-commerce platform connecting informal retailers to FMCG manufacturers, fixing stock-outs and logistics.

- How They Do It: They operate a massive logistics network. However, the model has pivoted. Recognizing that logistics is a low-margin, capital-intensive game, they are shifting to Fintech. They use the trading data of 450,000 merchants to offer working capital loans. The merger with MaxAB consolidates operations across East and North Africa to achieve economies of scale and centralized tech costs.19

Rank 3: d.light

- Annual Revenue (Est.): $309M.21

- Trajectory: Stable growth; heavily reliant on securitization.

- What They Do: Design and distribution of solar home systems and inverters.

- How They Do It: Similar to M-KOPA but with a stricter focus on energy hardware. Their competitive advantage lies in their financial engineering; they recently closed a $176M securitization facility, allowing them to recycle capital faster than competitors. They have provided energy to millions, leveraging the PAYG model to manage credit risk.1

Rank 4: Sun King (formerly Greenlight Planet)

- Annual Revenue (Global/Kenya): $250M+ (Global revenue implies substantial Kenya contribution as HQ).23

- Trajectory: Profitable; aggressive expansion into manufacturing.

- What They Do: The world’s largest off-grid solar energy company.

- How They Do It: Unlike competitors who often white-label hardware, Sun King is vertically integrated from design to distribution. They are currently establishing a local manufacturing plant in Nairobi to reduce import duties and FX exposure, a strategic move that will improve gross margins. Their $156M securitization in 2024 confirms the quality of their loan book.15

Rank 5: Watu Credit

- Annual Revenue: $231M (2024 Audited).25

- Trajectory: 67% revenue growth, though net profit dropped 85% due to rising costs.26

- What They Do: Asset financing for the gig economy, primarily bodabodas (motorcycles) and increasingly smartphones.

- How They Do It: Watu dominates the two-wheeler financing market through speed. They can approve a loan in hours. Their recovery infrastructure is their moat—utilizing GPS tracking and a network of recovery agents to maintain repayment discipline. They are pivoting aggressively to smartphones (1.4 million financed) as a lower-risk asset class compared to motorcycles.25

Rank 6: Kyosk Digital

- Annual Revenue (Est.): $142M.27

- Trajectory: High growth (145% CAGR).

- What They Do: A digital-first distribution platform for informal retailers.

- How They Do It: Kyosk focuses on data-driven distribution. Unlike Wasoko’s aggressive pan-African expansion, Kyosk has focused on depth and density in Kenya, leading to better unit economics. They connect retailers directly to manufacturers, cutting out middlemen and passing savings to the dukas (shops).

Rank 7: Cellulant

- Annual Revenue (Est.): $112M.17

- Trajectory: Achieved profitability in March 2024.29

- What They Do: The "plumbing" of African payments.

- How They Do It: Cellulant aggregates payment methods (mobile money, banks, cards) for global merchants (like Google, Booking.com) and local banks. Their strategic pivot from a consumer-facing app (Tingg) to pure B2B infrastructure was the catalyst for their turnaround to profitability. They process millions of transactions, taking a small slice of the volume.

Rank 8: Pula Advisors

- Annual Revenue (Est.): ~$106M.30

- Trajectory: Growing rapidly, evidenced by a $20M Series B.

- What They Do: Agricultural insurance and digital advisory for smallholder farmers.

- How They Do It: Pula doesn't sell directly to farmers. They use an "embedded" model, selling insurance through fertilizer companies, governments, and NGOs. If a farmer buys a bag of seed, insurance is included. This eliminates customer acquisition costs (CAC). They use satellite data and yield index modeling to automate claims, making micro-insurance viable.

Rank 9: BasiGo

- Annual Revenue (Est.): $64M.31 (Note: This likely represents Total Contract Value or Order Book given the fleet size of ~100 buses. Realized GAAP revenue is likely lower, but the order book supports the valuation).

- Trajectory: High capital intensity, nascent revenue recognition.

- What They Do: Electric bus assembly and leasing.

- How They Do It: Pay-As-You-Drive (PAYD). BasiGo decouples the battery cost from the bus cost. Operators pay a deposit similar to a diesel bus, then pay a mileage fee (e.g., KES 20/km) that covers electricity, maintenance, and the battery lease. This removes the upfront CAPEX barrier for Public Service Vehicle (PSV) operators.

Rank 10: Mogo Kenya

- Annual Revenue: ~$50M (Extrapolated from parent Eleving Group data).33

- Trajectory: Steady, profitable parent company.

- What They Do: Auto-lending (used cars) and logbook loans.

- How They Do It: Mogo targets a slightly more formal demographic than Watu, focusing on car financing and lending against vehicle logbooks. Their model relies on the liquidity of the used car market in Kenya, allowing them to quickly liquidate collateral in case of default.

4. Sectoral Alpha: The Next 5 Years (2025–2030)

Investing in 2025 requires looking beyond the "App layer" to the "Infrastructure layer." The easy money in simple payment apps has been made. The next wave of value creation will come from solving physical inefficiencies using digital rails.

4.1 Best Sectors for Investment

1. Cleantech & E-Mobility (The "Electron Arbitrage")

- Investment Thesis: Kenya's grid is 90% renewable (geothermal/hydro). This creates a unique arbitrage opportunity: using cheap, green domestic electrons to displace expensive, imported fossil fuels.

- Mathematical Support: A liter of petrol costs ~$1.50. The equivalent energy in electricity costs ~$0.30. The $1.20 spread is the Total Addressable Market (TAM) per liter replaced. With the Nairobi transport sector consuming millions of liters daily, the TAM is in the billions.

- Startup Gap: Independent Charging Infrastructure. Currently, BasiGo and Roam build their own charging depots. The market needs a "Tower Company" model for EV charging—an independent operator of charging hubs that serves all fleets, creating network effects.34

2. Embedded Fintech (The "Invisible Bank")

- Investment Thesis: Standalone payment apps are saturated. The opportunity lies in embedded finance—insurance inside a fertilizer app (Pula), credit inside a supply chain app (Jahazii), or payments inside a hospital system (M-Tiba).

- Growth Forecast: The African Buy-Now-Pay-Later (BNPL) market is projected to grow at a 14.8% CAGR to reach $10.63 billion by 2030.35

- Startup Gap: Credit Scoring as a Service. A centralized API that aggregates data from M-PESA, CRBs, and gig-platforms to provide a unified credit score for the informal sector.

3. Agri-Infrastructure (Cold Chain & Processing)

- Investment Thesis: 37-50% of food in Kenya is lost post-harvest.36 Startups that build physical cold storage or virtual aggregators will unlock massive value by converting "waste" into "inventory."

- Market Size: The cold chain market is projected to reach $250M by 2030, growing at a 10% CAGR.36

- Startup Gap: "Cooling-as-a-Service" (CaaS). Solar-powered cold rooms at aggregation centers (like markets in Karatina or Meru) where farmers pay per crate/day. This converts CAPEX into OPEX for the farmer.

5. The "Big Thing" (2025-2035): Green Compute & AI Infrastructure

The defining opportunity of the next decade is the convergence of Artificial Intelligence's hunger for power and Kenya's abundance of Geothermal energy.

The Thesis: Exporting "Green Compute"

Global AI models require massive data centers. Training a single Large Language Model (LLM) consumes gigawatt-hours of electricity. The developed world (US, Europe) is running out of grid capacity and facing strict carbon emission caps. Kenya has 10 Gigawatts (GW) of untapped geothermal potential in the Rift Valley.37

The Mechanism

Instead of exporting raw coffee or tea, Kenya will export "Green Compute." Data centers will be built at the source of power (geothermal wells in Olkaria/Naivasha), eliminating transmission losses. Global tech giants will lease this compute power to train their models sustainably.

Evidence of the Shift

- The Signal: The $1 billion partnership between Microsoft and G42 (UAE) to build a geothermal-powered data center in Kenya.38 This is the largest digital investment in Kenya's history.

- The Project: EcoCloud and G42 are developing a 1GW capacity data center campus. The initial phase is 100MW.39

- Strategic Advantage: Geothermal provides baseload power (24/7), unlike solar or wind which require expensive battery storage. This is critical for data center uptime tiers (Tier III/IV).

Startup Opportunities in this Ecosystem

Edge Data Centers: Smaller facilities in urban centers to handle latency-sensitive inference tasks.

AI Data Labeling: "Data Factories" employing youth to annotate datasets for Swahili/African language LLMs, bridging the gap in AI training data.

Data Center Support Services: Cooling technologies, physical security, and fiber maintenance for these massive facilities.

6. Global Capital Trends Extrapolated to Kenya

The global venture landscape is shifting, and these trends are manifesting in Kenya with specific local nuances.

6.1 From Venture Capital to Private Equity (PE)

Globally, IPO exits are drying up. In response, PE firms are buying out VC-backed scale-ups. In Kenya, this is visible in the Wasoko-MaxAB merger, a classic PE-style consolidation play to improve margins and dominance.

- Prediction: We will see more M&A consolidation in fragmented sectors like ISPs (Mawingu/Poa Internet) and Digital Credit providers. Investors should position for trade sales rather than IPOs on the NSE or NASDAQ.40

6.2 The Rise of "Deep Tech" and Hard Assets

Deep Tech funding in Africa surged by 130% between 2015 and 2023.41 Investors are favoring companies with defensible IP and physical moats (like manufacturing plants) over easily replicable software wrappers.

- Kenya Context: Sun King’s new manufacturing plant and Roam’s assembly lines are prime examples. The "moat" is no longer code; it is the factory and the distribution fleet.

6.3 Carbon Markets as a Revenue Layer

Global companies need high-quality carbon credits. Kenyan startups are embedding carbon revenue into their models.

- Example: KOKO Networks and BasiGo generate credits by displacing charcoal and diesel. This creates a secondary, USD-denominated revenue stream that can be securitized, effectively subsidizing the cost of hardware for the end consumer.42

7. Mathematical Substantiation & Value Chain Gaps

To invest intelligently, we must look at the unit economics.

7.1 Value Chain Gaps for Immediate Leverage

Gap 1: The "Mid-Mile" Cold Chain

- Problem: Farmers lose 50% of produce. Exporters have cold chain; domestic markets do not.

- Solution: Solar-powered cold storage at aggregation points.

- Math: A crate of tomatoes loses 30% value in 2 days due to heat. Cooling preserves 100% value. If cooling costs $0.50/crate/day and value saved is $5.00, the ROI is 10x.

Gap 2: Specialized Healthcare Logistics

- Problem: The KEMSA supply chain is inefficient, leading to stock-outs in public clinics.43

- Solution: "Maisha Meds for Public Health." A digital logistics layer that gives private pharmacies access to aggregated procurement, reducing drug costs by 20-30%.

Gap 3: Construction Material Supply Chain

- Problem: Construction costs are high due to waste (10-15%) and theft.

- Solution: A B2B marketplace for construction materials (like a "Wasoko for Cement") that enforces transparency and manages just-in-time delivery to sites, reducing waste and theft.44

8. Strategic Outlook & Conclusion

The era of the "copy-paste" Silicon Valley app is over in Kenya. The market has rejected solutions that do not solve fundamental, physical problems. The next 5-10 years belong to the Integrators—companies that combine hardware, software, and financing to address energy access, food security, and transport efficiency.

Key Recommendations for Investors:

Follow the Geothermal: Invest in the ecosystem surrounding the Naivasha/Olkaria data center corridor. This is the future industrial heart of East Africa.

Back the Securitizers: Companies like Sun King and M-KOPA that can tap into global debt markets have an infinite runway compared to equity-dependent firms. They are the new "Banks."

Prioritize Vertical Integration: Victory Farms and Sun King prove that owning the whole chain—from manufacturing/production to the final customer—is the only way to protect margins in a fragmented market.

Kenya is transitioning from a frontier market to a laboratory for Sustainable Development. The "Big Money" will flow to those who build the rails—physical and digital—for this Green Digital Economy.

About the author

Mr. Derrick Macharia

AI Engineer @Pawanax

Related articles

Business

A comprehensive Analysis of Kenya's Economy

There is a comforting myth many developing countries tell themselves: “What happens in Washington is far away. We have our own problems.” Kenya, like most emerging economies, knows this is not true — but still underestimates how deeply American fiscal de...

Mr. Derrick Macharia

December 13, 2025 · 5 min read

Business

How the World Quietly Crossed the Point of No Return

The Event Horizon of 2025 History rarely announces itself. It does not arrive with trumpets, declarations, or a single catastrophic day that future textbooks can easily circle in red. Instead, it moves through infrastructure, balance sheets, food systems...

Mr. Derrick Macharia

January 10, 2026 · 5 min read

Business

The best AI companies in Kenya

Unlocking the Trillion-Dollar Potential of Kenya’s Sovereign AI Revolution (2025-2030) 1. The Tectonic Shift in the Silicon Savannah The narrative of African technology has, for the better part of two decades, been monopolized by a single story: Fintech....

Mr. Derrick Macharia

December 12, 2025 · 5 min read

Stay in the loop

Get new articles on healthcare AI and African health systems.

Healthcare AI insights. Unsubscribe anytime.